This guide is part of our Current Real Estate Market Insights → [Current Real Estate Market Insights ]

Interest rate movements have reshaped the Denver-area housing market by altering affordability thresholds, slowing seller turnover, and handing buyers more leverage in negotiations. Current rates in the 6.5–7% range—more than double the lows of 2020–2021—directly impact monthly payments, forcing buyers to recalibrate budgets and prioritize total ownership costs amid Colorado’s high property taxes and maintenance demands. For serious buyers, sellers, and relocating homeowners, these shifts matter because they extend decision timelines, increase concession opportunities, and emphasize long-term value over short-term speculation in a region defined by commute patterns and weather-related expenses.

How Higher Rates Compress Buyer Budgets

Elevated rates reduce purchasing power by 20–30% compared to the 3% era, turning a $600,000 home from a $2,500 monthly principal-and-interest payment to over $3,900 at 6.75%. This compression matters in the Denver metro, where median prices hold in the mid-$500,000s to low-$600,000s: buyers must now target smaller homes, condos, or suburbs like Centennial and Littleton to stay within reach, often sacrificing square footage or location premiums.

The psychological effect amplifies this: many first-time and move-up buyers pause, creating a demand pause that extends days on market and prompts price adjustments. Relocators from low-rate coastal markets underestimate the hit, as Denver’s 1–1.5% property taxes and insurance (elevated by fire and weather risks) add $800–$1,200 monthly beyond the mortgage.

The Lock-In Effect and Inventory Dynamics

Homeowners with sub-4% mortgages hesitate to list, fearing a payment shock that could exceed $1,500 monthly on equivalent properties. This “golden handcuff” limits supply in desirable areas like Highlands Ranch and Aurora, keeping inventory below historical norms but sufficient to tilt leverage toward buyers—active listings up 25–40% year-over-year across the metro.

For sellers, the implication is clear: only compelling moves (job changes, downsizing) trigger listings, leaving stale inventory for others. Buyers benefit from 40–60 days on market averages, time to inspect for Colorado-specific issues like foundation settling from clay soils or roof wear from snow loads.

Suburban Variations in Rate Sensitivity

Southwest suburbs (Littleton, Centennial) see sharper inventory gains due to family relocations, with townhomes softening most as buyers avoid stretch financing. Eastside Aurora holds firmer, appealing to affordability seekers despite longer commutes via I-225 to DTC (20–30 minutes). Highlands Ranch balances with metro district taxes that rates exacerbate, pushing buyers toward concessions.

Negotiation Leverage from Rate-Driven Caution

Higher rates foster buyer selectivity: fewer waive inspections or rush bids, leading to 20–30% of listings with price cuts averaging 3–5%. Common wins include seller-paid buydowns (reducing effective rates by 0.5–1%) or $10,000–$20,000 credits, directly offsetting rate impacts without appraisal risks.

Sellers adapt by pricing to 95–98% of comps, using recent sold data over 2022 peaks. In this environment, homes staged for modern needs—main-floor offices, energy-efficient updates—move faster, as buyers view purchases through a 7–10 year lens.

Affordability Stress and Ownership Cost Realities

Denver-area buyers face layered costs that rates magnify: Arapahoe/Douglas County taxes at 1.1–1.4%, HOAs ($200–$500/month in planned communities), and maintenance ($0.01–$0.02/sq ft annually for freeze-thaw repairs). A $650,000 Centennial home at 6.75% totals $5,200–$6,000 monthly including extras—28–35% of median household income—straining qualification ratios.

Relocators must model scenarios: fixed-rate stability versus ARM risks if rates fall. Utilities run 15–20% above national averages due to heating demands, underscoring why buyers prioritize efficient 2000s+ stock over older ranches needing HVAC overhauls.

Rate Decline Scenarios and Market Responses

Prospective Fed cuts could lower 30-year fixeds to 5.5–6% by mid-2026, unlocking pent-up supply and compressing buyer windows. Early movers now capture equity before appreciation resumes (forecast 2–4% annually), while waiting risks bidding wars on limited foothill-adjacent inventory.

Sellers timing exits weigh holding costs against potential refi relief for buyers. Data suggests gradual declines favor prepared participants over speculators.

Commute and Location Choices Under Rate Pressure

Rates sharpen focus on transport efficiency: C-470 corridors (Centennial to Highlands Ranch) minimize DTC commutes (10–15 minutes), justifying premiums despite payments. Light rail extensions aid Aurora-Denver links, appealing to dual-income households capping budgets. I-25 variability pushes southwest preferences, where value per commute minute exceeds eastside volume.

Strategies for Buyers in a Rate-Sensitive Market

Thoughtful approaches maximize positioning:

- Secure rate locks or buydowns on 30+ DOM listings, targeting 45–60 day concessions.

- Stress-test at 7.5% + 1% rate buffer, factoring metro taxes and 1% annual maintenance.

- Prioritize functional layouts (3 beds, 2 baths, garage) in B+ locations over A- condition in C spots.

FHA/VA options ease entry for first-timers, with sellers covering PMI offsets.

Strategies for Sellers Amid Buyer Rate Caution

Position defensively:

- Disclose rate-friendly incentives upfront to attract qualified traffic.

- Preempt inspections for structural items strained by Colorado weather.

- Target spring listings if holding low-rate equity, aligning with potential cuts.

Visualizing Rate Impact on Denver Affordability

Denver metro median prices stable near $575,000 pair with rising rates to flatten affordability, as prior charts showed slight price softening amid inventory

Elevated rates reduce purchasing power by 20–30% compared to the 3% era, turning a $600,000 home from a $2,500 monthly principal-and-interest payment to over $3,900 at 6.75%. This compression matters in the Denver metro, where median prices hold in the mid-$500,000s to low-$600,000s: buyers must now target smaller homes, condos, or suburbs like Centennial and Littleton to stay within reach, often sacrificing square footage or location premiums.

The psychological effect amplifies this: many first-time and move-up buyers pause, creating a demand pause that extends days on market and prompts price adjustments. Relocators from low-rate coastal markets underestimate the hit, as Denver’s 1–1.5% property taxes and insurance (elevated by fire and weather risks) add $800–$1,200 monthly beyond the mortgage.

The Lock-In Effect and Inventory Dynamics

Homeowners with sub-4% mortgages hesitate to list, fearing a payment shock that could exceed $1,500 monthly on equivalent properties. This “golden handcuff” limits supply in desirable areas like Highlands Ranch and Aurora, keeping inventory below historical norms but sufficient to tilt leverage toward buyers—active listings up 25–40% year-over-year across the metro.

For sellers, the implication is clear: only compelling moves (job changes, downsizing) trigger listings, leaving stale inventory for others. Buyers benefit from 40–60 days on market averages, time to inspect for Colorado-specific issues like foundation settling from clay soils or roof wear from snow loads.

Suburban Variations in Rate Sensitivity

Southwest suburbs (Littleton, Centennial) see sharper inventory gains due to family relocations, with townhomes softening most as buyers avoid stretch financing. Eastside Aurora holds firmer, appealing to affordability seekers despite longer commutes via I-225 to DTC (20–30 minutes). Highlands Ranch balances with metro district taxes that rates exacerbate, pushing buyers toward concessions.

Negotiation Leverage from Rate-Driven Caution

Higher rates foster buyer selectivity: fewer waive inspections or rush bids, leading to 20–30% of listings with price cuts averaging 3–5%. Common wins include seller-paid buydowns (reducing effective rates by 0.5–1%) or $10,000–$20,000 credits, directly offsetting rate impacts without appraisal risks.

Sellers adapt by pricing to 95–98% of comps, using recent sold data over 2022 peaks. In this environment, homes staged for modern needs—main-floor offices, energy-efficient updates—move faster, as buyers view purchases through a 7–10 year lens.

Affordability Stress and Ownership Cost Realities

Denver-area buyers face layered costs that rates magnify: Arapahoe/Douglas County taxes at 1.1–1.4%, HOAs ($200–$500/month in planned communities), and maintenance ($0.01–$0.02/sq ft annually for freeze-thaw repairs). A $650,000 Centennial home at 6.75% totals $5,200–$6,000 monthly including extras—28–35% of median household income—straining qualification ratios.

Relocators must model scenarios: fixed-rate stability versus ARM risks if rates fall. Utilities run 15–20% above national averages due to heating demands, underscoring why buyers prioritize efficient 2000s+ stock over older ranches needing HVAC overhauls.

Rate Decline Scenarios and Market Responses

Prospective Fed cuts could lower 30-year fixeds to 5.5–6% by mid-2026, unlocking pent-up supply and compressing buyer windows. Early movers now capture equity before appreciation resumes (forecast 2–4% annually), while waiting risks bidding wars on limited foothill-adjacent inventory.

Sellers timing exits weigh holding costs against potential refi relief for buyers. Data suggests gradual declines favor prepared participants over speculators.

Commute and Location Choices Under Rate Pressure

Rates sharpen focus on transport efficiency: C-470 corridors (Centennial to Highlands Ranch) minimize DTC commutes (10–15 minutes), justifying premiums despite payments. Light rail extensions aid Aurora-Denver links, appealing to dual-income households capping budgets. I-25 variability pushes southwest preferences, where value per commute minute exceeds eastside volume.

Strategies for Buyers in a Rate-Sensitive Market

Thoughtful approaches maximize positioning:

- Secure rate locks or buydowns on 30+ DOM listings, targeting 45–60 day concessions.

- Stress-test at 7.5% + 1% rate buffer, factoring metro taxes and 1% annual maintenance.

- Prioritize functional layouts (3 beds, 2 baths, garage) in B+ locations over A- condition in C spots.

FHA/VA options ease entry for first-timers, with sellers covering PMI offsets.

Strategies for Sellers Amid Buyer Rate Caution

Position defensively:

- Disclose rate-friendly incentives upfront to attract qualified traffic.

- Preempt inspections for structural items strained by Colorado weather.

- Target spring listings if holding low-rate equity, aligning with potential cuts.

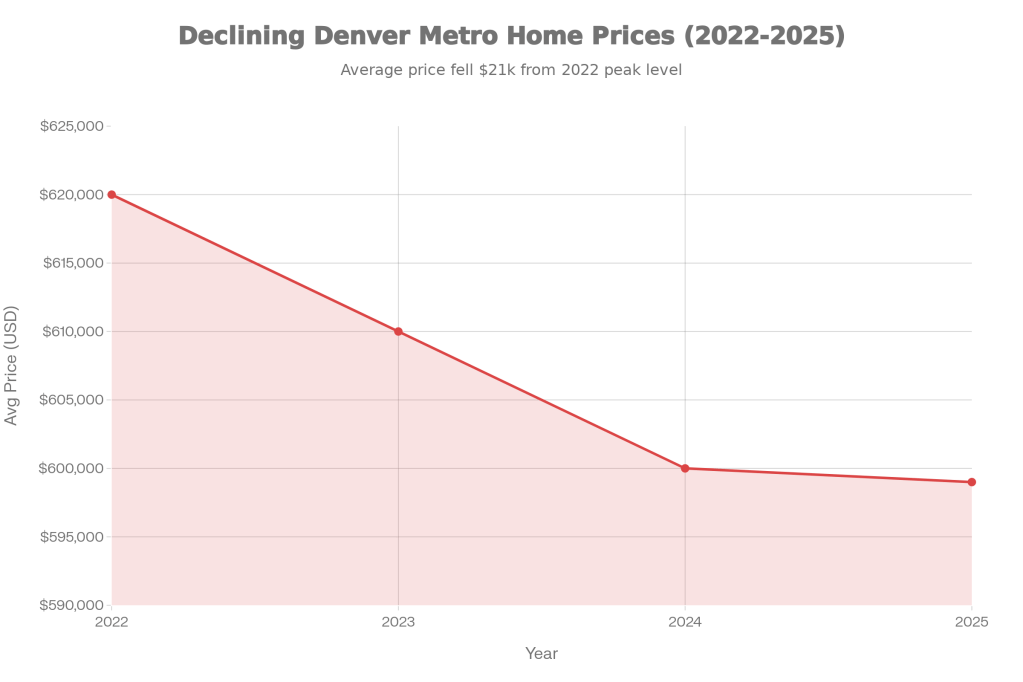

Visualizing Rate Impact on Denver Affordability

Denver metro median prices stable near $575,000 pair with rising rates to flatten affordability, as prior charts showed slight price softening amid inventory growth. This equilibrium rewards disciplined moves.

Denver Metro Average Home Price Trend, 2022–2025 (Approximate)

Long-Term Perspective on Rates and Value

Rates above 6% normalize cycles, filtering noise to favor assets with durable demand: strong schools (Littleton 27J), job corridors (DTC), and resilient builds. Equity builds steadily for 10-year holders, outpacing rents amid 3–5% annual increases.

Navigating Denver-Area Rates Strategically

Interest rate movements create a deliberate market where preparation determines outcomes: buyers negotiate total costs, sellers price to comps, and relocators align with commutes and stock realities. Fundamentals—job growth, constrained land—sustain value through volatility.

Reach out to the authoring agent today for personalized rate scenarios, affordability modeling, and market-specific guidance tailored to your Denver-area buying, selling, or relocation plans.

How Long It Takes Homes to Sell in Different Denver Suburbs

This guide is part of our Current Real Estate Market Insights → [Current Real Estate Market Insights ] Denver suburbs exhibit distinct selling timelines shaped by inventory levels, school districts, commute access, and local housing stock, with current medians ranging from 25 days in high-demand areas to 60+ in cooling pockets. These variations matter because longer…

What Happens to the Market After the Holidays

This guide is part of our Current Real Estate Market Insights → [Current Real Estate Market Insights ] Colorado’s real estate market moves distinctly with the seasons, influenced by weather patterns, school calendars, tax deadlines, and buyer relocation timing. These cycles matter because they create predictable windows of leverage for buyers and sellers, affecting negotiation power,…

Seasonal Real Estate Trends in Colorado: What to Expect

This guide is part of our Current Real Estate Market Insights → [Current Real Estate Market Insights ] Colorado’s real estate market moves distinctly with the seasons, influenced by weather patterns, school calendars, tax deadlines, and buyer relocation timing. These cycles matter because they create predictable windows of leverage for buyers and sellers, affecting negotiation power,…

Leave a comment